“கணக்கு சரிதான்னு நினைக்கிறோம்… ஆனா லாபம் ஏன் குறையுது?”

Let us start with a simple calculation that happens in many poultry trading businesses.

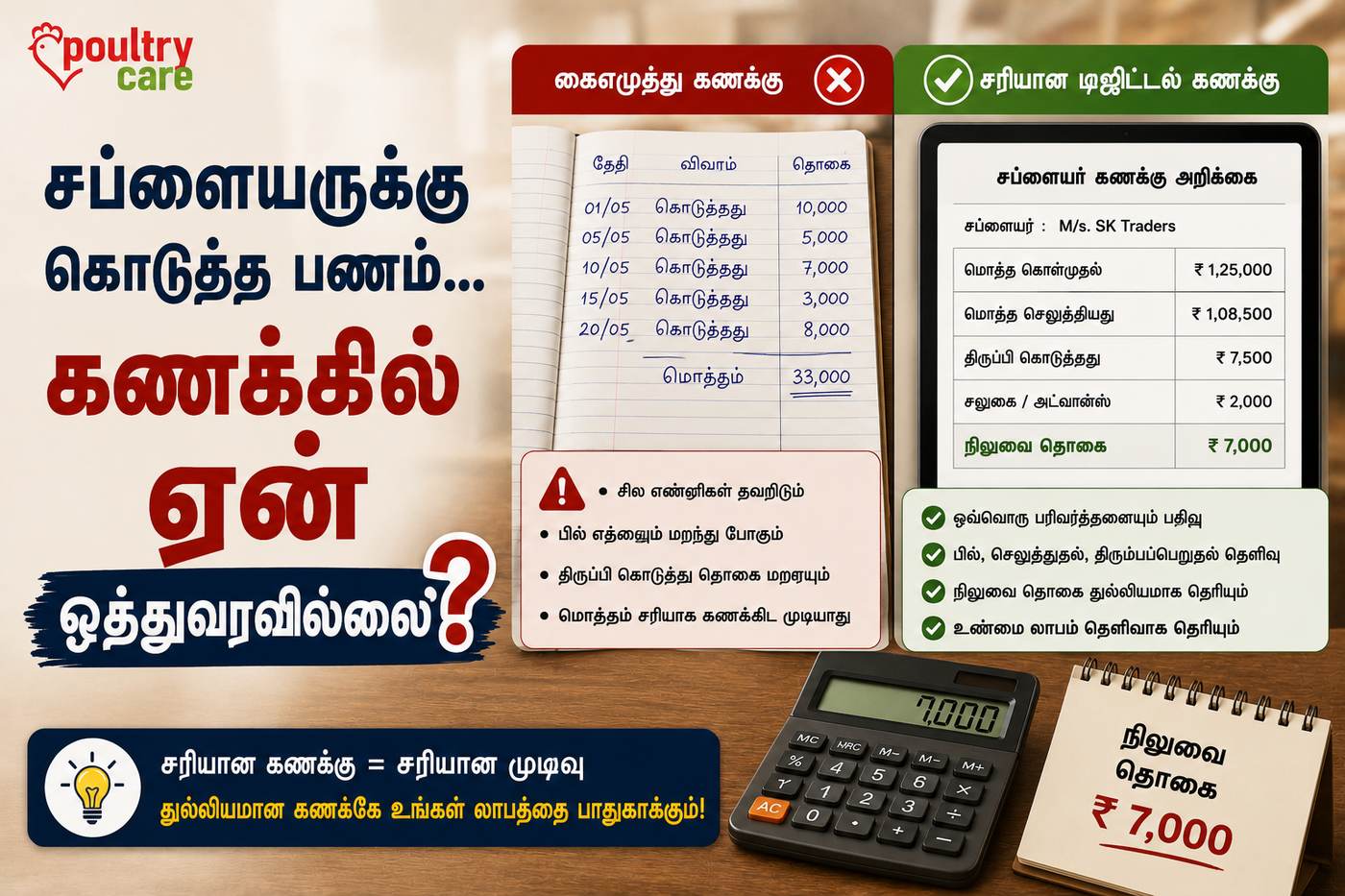

If you miss recording just 1,000 of daily expenses, in 25 working days the missing amount becomes 25,000. In six months, this turns into 1.5 lakh. This money is not stolen, not lost physically, but simply forgotten in records.

Most traders feel accounts are correct because books are closed. But closed books do not always mean correct profit. This is how accounting mistakes quietly reduce profit without creating noise.

Why Accounting Is Treated as a Month-End Job

In many trading setups, accounting is done only at the end of the month. During daily operations, focus stays on buying, selling, transport, and collection. Expenses are noted loosely or remembered later.

When accounting is delayed, small mistakes pile up. Expenses get missed, entries get mixed, and memory replaces accuracy. By the time numbers are reviewed, it becomes difficult to trace where things went wrong.

Poultry trading moves fast. Accounting that moves slowly cannot keep up.

Mixing Personal and Business Expenses

One of the most common accounting mistakes in poultry trading is mixing personal and business expenses. Fuel, phone bills, vehicle repair, and even food expenses often get paid from the same pocket.

When expenses are mixed, profit becomes unclear. Traders feel business is not earning enough, but in reality, business money is being used unknowingly for personal needs.

This habit slowly weakens financial discipline and creates confusion in profit calculation.

Wrong Valuation of Stock and Weight

Accounting errors also happen when stock and weight are valued incorrectly. Purchase weight, sale weight, and remaining stock are sometimes recorded based on assumption instead of actual measurement.

Even small mistakes in weight valuation change profit numbers significantly. When stock value is wrong, profit shown in accounts is also wrong. Traders may think margin is low due to market conditions, while the real issue is incorrect accounting.

Delayed Entry of Expenses and Sales

Many traders record expenses and sales after several days. During this gap, details are forgotten or estimated. Transport costs, loading charges, and small cash expenses are often missed or rounded off.

Delayed entries create delayed awareness. When traders do not see daily cost clearly, they cannot control it. Accounting becomes reactive instead of supportive.

How Accounting Confusion Affects Decision-Making

When accounts are not clear, decisions become weak. Traders hesitate to invest, expand, or negotiate confidently. They are unsure whether the business is actually profitable.

This confusion creates stress. Traders work harder but feel less confident. Over time, they lose trust in their own numbers.

Clear accounting is not about paperwork. It is about confidence and clarity.

What Changes When Accounting Becomes Simple and Regular

When traders start recording expenses, sales, and stock regularly, clarity improves. Profit numbers start making sense. Losses become visible early.

Accounting becomes a daily habit, not a monthly burden. Traders feel more in control. Decisions become calm and planned instead of rushed.

Conclusion: Profit Is Lost More in Records Than in Market

In poultry trading, profit does not disappear only because of market conditions. It often disappears due to small accounting mistakes made daily.

Correct accounting does not require complex knowledge. It requires honesty, discipline, and regular attention. When accounts reflect reality, profit reflects reality.

The day accounting becomes clear is the day trading becomes confident. And confident traders build stronger, longer-lasting businesses.